.webp)

The One Big Beautiful Bill: A Gut Punch, But Not a Knockout for Climate Tech

The One Big Beautiful Bill Act (OBBB) was signed into law by President Trump on July 4, 2025. This act is President Trump’s signature energy reform and is a sweeping rewrite of U.S. clean-energy policy. The bill slashes or eliminates dozens of key incentives, ramps up critical sourcing rules, and raises energy costs for American households. Climate advocates were quick to warn of dire consequences. And while they’re not wrong to sound the alarm, it’s important to keep perspective. The OBBB undoubtedly hurts the climate tech industry, but it doesn’t veer us off-course entirely. If anything, it highlights why building politically resilient climate solutions matters now more than ever.

A Broadside Against the IRA

The Inflation Reduction Act (IRA), former President Biden’s climate and energy policy, stands as the most significant U.S. investment in clean energy to date. It delivered clean energy tax credits, consumer incentives, and manufacturing support that turbocharged renewables deployment, reshored clean-tech supply chains, and electrified homes and transportation.

But OBBB unravels some of that progress, most notably:

- Eliminating the federal tax credits for residential solar, energy efficiency retrofits, and home electrification (25D and 25C) starting as soon as the end of 2025.

- Sunsetting the clean vehicle tax credits for both new and used EVs (30D and 25E) by September 2025.

- Terminating wind and solar tax credits as part of the technology-neutral credits for zero emission technology (45Y and 48E).

Furthermore, OBBB is fundamentally bad for the environment and American’s wallets. The Princeton REPEAT Project estimates OBBB will add 190 million metric tons of CO₂ emissions annually by 2030, or the equivalent to 41 million passenger vehicles. In addition, a report from Energy Innovation projects that household energy bills would more than double in some states by 2030. Together, these data show a sharp reversal of IRA gains.

Solar, Wind, and the Race Against Time

Among the hardest hit sectors are solar and wind. Under the IRA, these technologies had multi-year certainty with the 45Y/48E framework giving investors confidence to plan projects well into the next decade.

The OBBB reverses that certainty. It accelerates the expiration of the investment tax credit (ITC) and production tax credit (PTC), requiring projects to begin construction by mid-2026 or be in service by the end of 2027 to qualify. That’s an incredibly tight timeline for utility-scale projects that routinely face two- to three-year delays in permitting, interconnection, and supply chain logistics. With the race to power AI, these interconnection queues are as long as seven years.

Estimates show a reduction in cumulative capacity additions of 140 GW of solar and 160 GW of wind through 2035. This is significant, especially considering the reduction in solar is equal to roughly 56% of current solar capacity. Cuts like these jeopardize grid resiliency, impede energy supply for power hungry data centers, and slow the clean energy transition.

Advanced Manufacturing: Progress Meets Politics

One of the IRA’s goals was reshoring clean tech supply chains. The 45X credit, which incentivized domestic production of solar panels, batteries, and inverters, is largely untouched by the OBBB, with a few exceptions: i) wind; ii) sourcing materials from foreign entities of concern, a thinly veiled reference to China; iii) the phase out of critical minerals, which potentially discourages long-term investment in new projects, iv) and adds metallurgical coal to the eligibility list of critical minerals.

While national security concerns about clean tech dependence on China are valid, the bill's new compliance hurdles risk kneecapping domestic projects before U.S.-based manufacturing has had time to mature. Instead of encouraging an orderly transition, the bill may simply push developers to shelve projects or rely on more expensive components.

And let’s be clear: China is undoubtedly winning the global clean energy race. It produces over 80% of the world’s solar modules, dominates EV battery production, and controls much of the global refining capacity for lithium, cobalt, and rare earth elements. The IRA’s industrial policy was an attempt to counterbalance that dominance.

Consumers Lose, Too

Beyond the macroeconomic and climate impacts, the OBBB hits American consumers hard. The repeal of residential energy incentives will raise the cost of home electrification, solar installations, and efficient appliance upgrades. That will disproportionately impact low- and middle-income households.

And as noted, energy bills are expected to climb significantly. According to Energy Innovation, the average household could see hundreds of dollars in increased costs annually, largely due to increased reliance on fossil fuels and slower adoption of cost-saving clean energy technologies.

But It’s Not All Bad News

Despite the above, the clean energy transition is not dead. In fact, there are several bright spots in the bill and in the market that give us reason for optimism.

- The OBBB retains the expanded tax credits for nuclear energy and advanced geothermal, two technologies that are poised to play a critical role in deep decarbonization. These sectors are still nascent, and their inclusion in the bill reflects growing bipartisan recognition of their importance.

- Energy storage remains eligible for the full investment tax credit through 2033, along with one-year bonus depreciation. Batteries are key to unlocking more wind and solar on the grid. With strong long-term tailwinds, including AI-driven demand growth and a capacity-constrained grid, storage still has momentum.

- Individuals are losing the EV tax credit, but fleet and commercial adoption continues accelerating, driven by operational savings and regulatory standards. Auto OEM roadmaps remain locked toward zero emissions. Despite the expected rollbacks from OBBB, BloombergNEF is still expecting significant global growth in EVs in 2025 and modest growth in the US.

- Critical minerals get a boost of approximately $7.5B across a few different funds, including Industrial Base Fund’s carve out for investments in critical mineral supply chains, the National Defense Stockpile Transaction Fund for critical minerals, and the DoD’s Office of Strategic Capitals carve out for critical minerals.

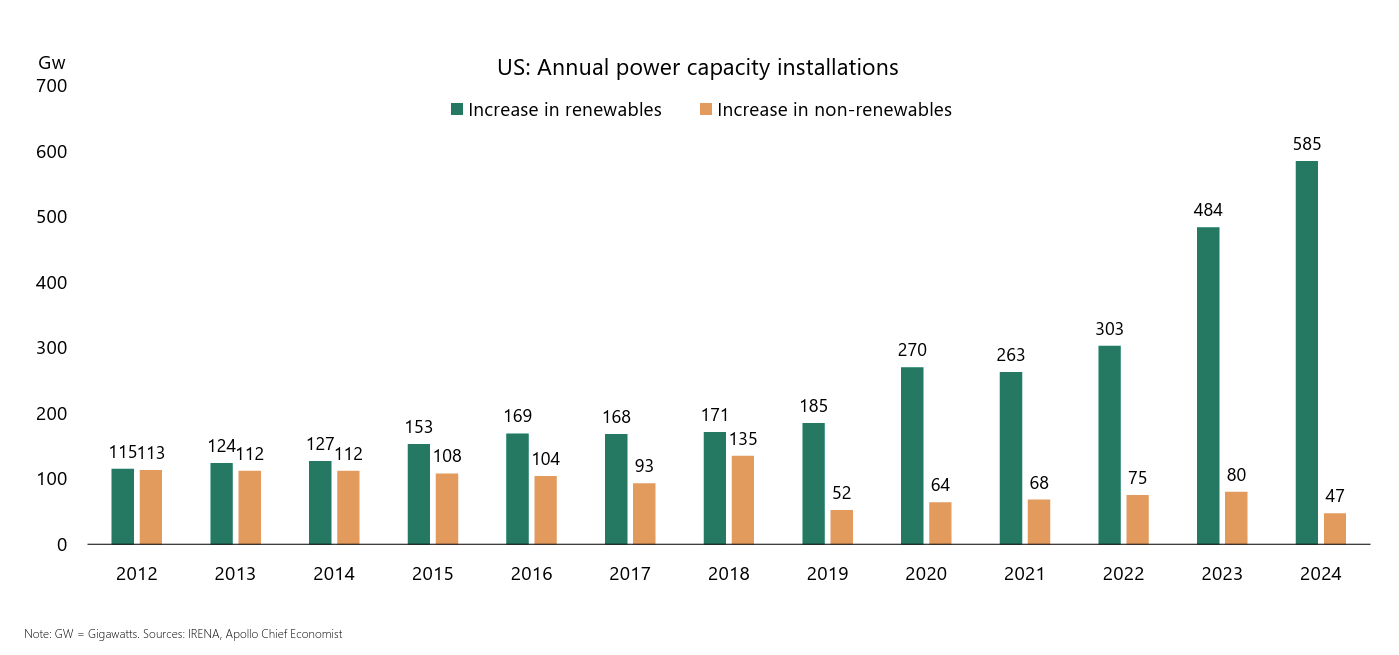

- Even with subsidy rollbacks, many clean energy technologies are simply too competitive to ignore. The cost of utility-scale solar has fallen by over 80% in the last decade. Wind and solar remain the cheapest sources of new generation in most U.S. markets. As reported by Apollo, more than 90% of US power capacity installations are renewables.

The Bigger Picture: Speed, Resilience, and AI

Looking ahead, market competitive climate tech technologies must continue to mature, agnostic of federal policy support. At Buoyant Ventures, we’ve always backed asset-light companies that don’t depend on government subsidies to scale. That discipline feels more important than ever.

There are also powerful market dynamics beyond policy that continue to drive the energy transition forward. One of the most consequential is load growth. After decades of relatively flat electricity demand in the United States, we're now entering a new era of rapid acceleration. Electricity demand is projected to grow as much as 25% by 2030, driven largely by compute-intensive workloads such as generative AI, bitcoin, reshoring of manufacturing, and electrification broadly. This surge creates a powerful, durable tailwind for utilities, developers, and distributed energy providers. With gas turbine backlogs of five years and interconnection queue backlogs of up to seven years, distributed power along with renewables and batteries are the cheapest, fastest, solution to meet this moment.

This also increases the focus on energy efficiency, or using less energy to power AI. At Buoyant we are looking for solutions across the AI infrastructure stack, like our portfolio company Ocient. Ocient built and commercialized a novel software architecture for data analytics, lowering costs alongside emissions for customers.

Another market trend is the need to optimize physical assets already in the ground given the barriers and timeline for building new energy capacity. Our solar software company, Raptor Maps, helps owners and operators of solar equipment identify repairs and other maintenance needed to squeeze out more energy from aging equipment.

"The OBBB act will have the effect of making financial returns for renewables harder to achieve and the bill brings two topics to the forefront for the solar industry. First is that developers and EPCs need to suddenly move much faster without sacrificing quality; second is that owners, operators, and asset managers must uncover double digit cost savings opportunities without reducing plant availability. Raptor Maps has been building for this moment with solutions that enable speed and cost savings at the required magnitude and pace. We have proven that our solutions lower annual O&M expense by 20%, for example. The OBBB comes at the time of our economy having a once in a generation step change in electricity demand, and so power projects will continue at a rapid rate and no power source can come to market with the same speed and cost effectiveness as solar". - James Wagstaff, CRO Raptor Maps

Uncertainty has been a core theme of 2025. AI solutions are a tool for energy stakeholders to manage this uncertainty. For example, our portfolio company Sunairio, which uses advanced weather analytics to derive net load forecasts, can help to manage grid instability. This is especially the case in supply constrained scenarios, which are more likely as a result of the OBBB. Similarly, HData, which provides energy regulatory intelligence, can help stakeholders to navigate any changes to regulation as a result of the OBBB.

The climate industry’s mission remains clear: scale solutions that are resilient, capital-efficient, and provide real business value beyond climate benefits. OBBB does not change that.

Final Thoughts

The One Big Beautiful Bill delivers a political and economic blow to the clean energy transition. It adds emissions, raises costs, delays capacity, and shakes investor confidence.

But it is not a knockout. Now is the time to double down on solutions that work in a federal incentive light world. That means software, data, efficiency, optimization. It means better project finance, faster interconnection, and smarter grid management. It means proving that climate innovation can be durable and is the future of the economy.

At Buoyant, we’re not slowing down. We’re backing the founders building that future.

Related Posts

Subscribe to stay updated on news, insights, & invites to special events within our community.

We’re lighting the path forward for the ClimateTech industry—keep up with us along the journey.