.webp)

Buoyant's 2026 Outlook

.png)

The last two years marked a step-function change in what’s possible with AI, but 2026 will be about what’s possible in the real world. The AI wave is forcing a return to fundamentals: electricity, grid capacity, supply chains, capex discipline, and security. For climate, this is reshaping the investing landscape in real time. Capital is concentrating into fewer, more competitive companies, and climate outcomes are increasingly being driven by industrial demand rather than policy ambition. As a climate tech and AI-focused fund, we see the convergence as unavoidable: AI is rapidly becoming one of the most important demand drivers for the grid, and the grid is quickly becoming one of the most important gating factors for AI. Against a backdrop of geopolitical uncertainty and rising physical constraints, 2026 will reward companies that can execute, and punish those built on fragile assumptions. These are Buoyant’s predictions for what comes next.

1) The Great Capitulation: Business Fundamentals Will Trump Politics ⚡🏛️

After a year of aggressive rhetoric, the federal government will be forced into an uneasy truce with renewables. However, this isn’t an ideological shift, but a surrender to physics and fiscal reality.

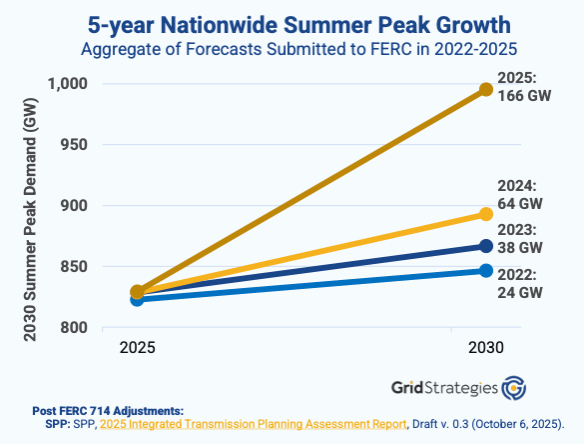

Electricity prices remain under pressure, the grid is increasingly constrained, and industrial expansion is pulling gigawatts of load into the system faster than traditional infrastructure can respond. Canary Media reports that 22GW of energy capacity is stuck in federal limbo while electricity prices increase and large commercial and industrial customers clamber for power. The EIA reported 10-28% average price increases for Eastern states like Maine, New Hampshire, Maryland, and Washington DC from Oct 2024 to Oct 2025.

Grid Strategies reported that peak load growth ballooned in 2025 based upon data center demand, industrial and manufacturing loads, and EV growth:

Renewables are increasingly treated as a pragmatic lever: one of the fastest deployable ways to bring incremental capacity online and avoid inflationary pressure from constrained power. As a result, the bottleneck is no longer whether projects happen, but whether they can clear interconnection queues and reach commercial operation on schedule. “Speed to power” is the battle cry.

We are already seeing legal victories for off-shore wind developers that were halted by federal injunctions. And while Buoyant was a little early in our 2025 prediction that data center developers would be building onsite generation to power their loads (Bring Your Own Power), we are seeing early signs that this is “becoming table stakes” as Google has said and is demonstrating with its acquisition of Intersect Power.

2026 takeaway: In the end, business fundamentals win. Market forces overwhelm ideology, and the winners will be the teams that can execute through permitting, interconnection, and procurement bottlenecks the fastest.

2) No Major US Correction for AI & Data Centers in 2026 — But the Financial & Power Plumbing Starts to Crack 🏗️⚡🫧

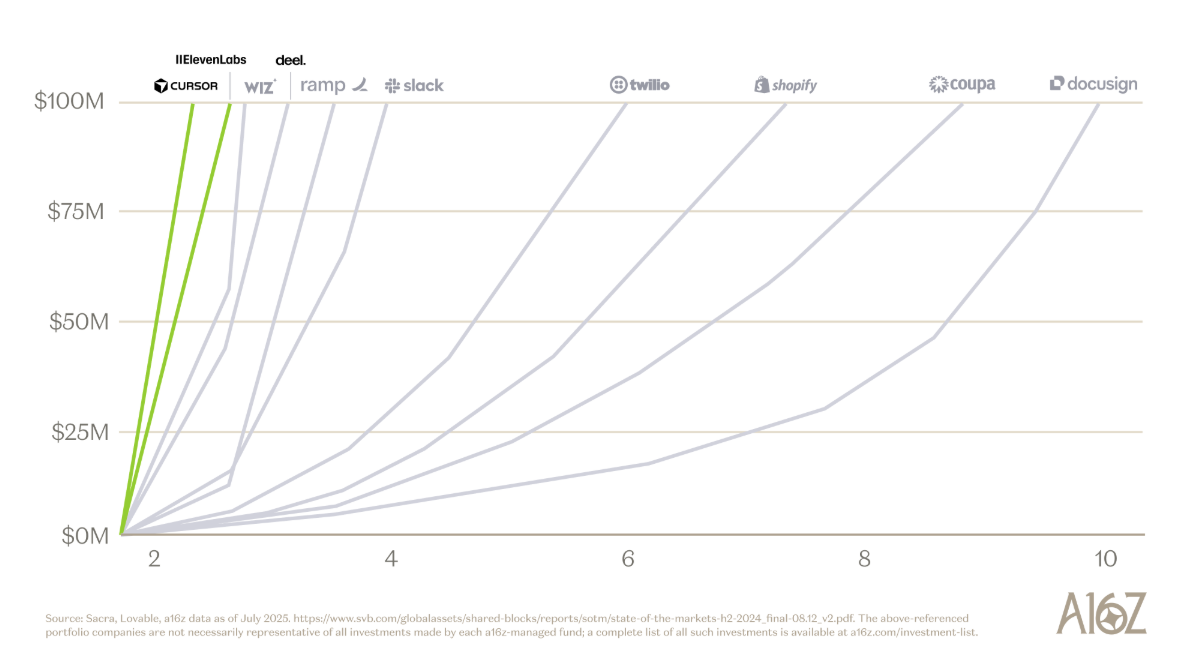

Despite the “bubble” narrative in 2025, we do not expect a major AI-driven market correction in 2026. Demand remains real, major players remain committed, and at least one large AI company going public could provide liquidity and renewed optimism. As seen in the chart below, AI revenues are growing faster than previous technologies.

That said, the physical and financial stresses behind this buildout are getting harder to ignore. In 2026, we expect the market to increasingly confront reinforcing forces:

- Interconnection and power delays continue to push timelines. Many projects scheduled for 2027–2028 will slip as grid upgrades, equipment lead times, and interconnection studies extend. The market will start to price execution risk more directly, even if demand stays strong.

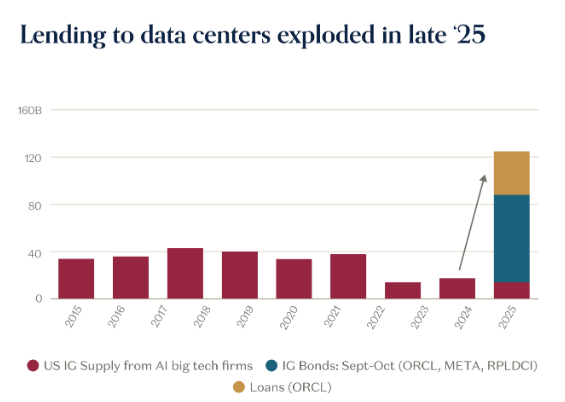

- Credit structures are getting stress-tested. A meaningful portion of 2025 infrastructure expansion was enabled by private credit and off-balance-sheet financing that assumed sustained high utilization and uninterrupted growth. The most visible example was Blue Owl’s $27B private-debt financing for the Hyperion campus, structured off Meta’s balance sheet. While we do not expect a high-profile default in 2026, the conditions that lead to a default begin forming here. The actual risk shows up later, as projects go live and underwriting assumptions collide with real ramp curves.

2026 takeaway: 2026 stays strong on demand and optimism, but the system starts to show strain. 2027–2028 is when power delays + leverage risk can combine into a sharper correction. However, efficiency gains (both in chips and in software optimization) mean the industry may be able to do more with less than many forecasts assume. For example, our recent investment in Hammerhead shows how existing data centers can unlock stranded power from within their grid allocations today. The danger isn’t underinvestment, it’s misallocated investment.

3) Overhyped AI Sectors Start to See Zeros 🧨🤖

Despite the above prediction that we do not expect a major AI-driven market correction in 2026, we do expect to see a meaningful number of AI companies fail. Foundational models are getting good enough fast (especially on reasoning, tool use, and multimodal workflows) and that is lowering differentiation for many application-layer startups. Google’s Gemini releases demonstrate how quickly core model providers are bundling more capability directly into the horizontal layer and are broadly accessible via API. Additionally OpenAI’s release of Sora was not only a capability step-change, but an example of bundled tools into the ChatGPT subscription stack which kills competition. Anthropic’s release of Claude Code made agentic workflows real for everyday developers. This evolving capability landscape makes it harder for startups to justify venture-scale valuations unless they have a real moat.

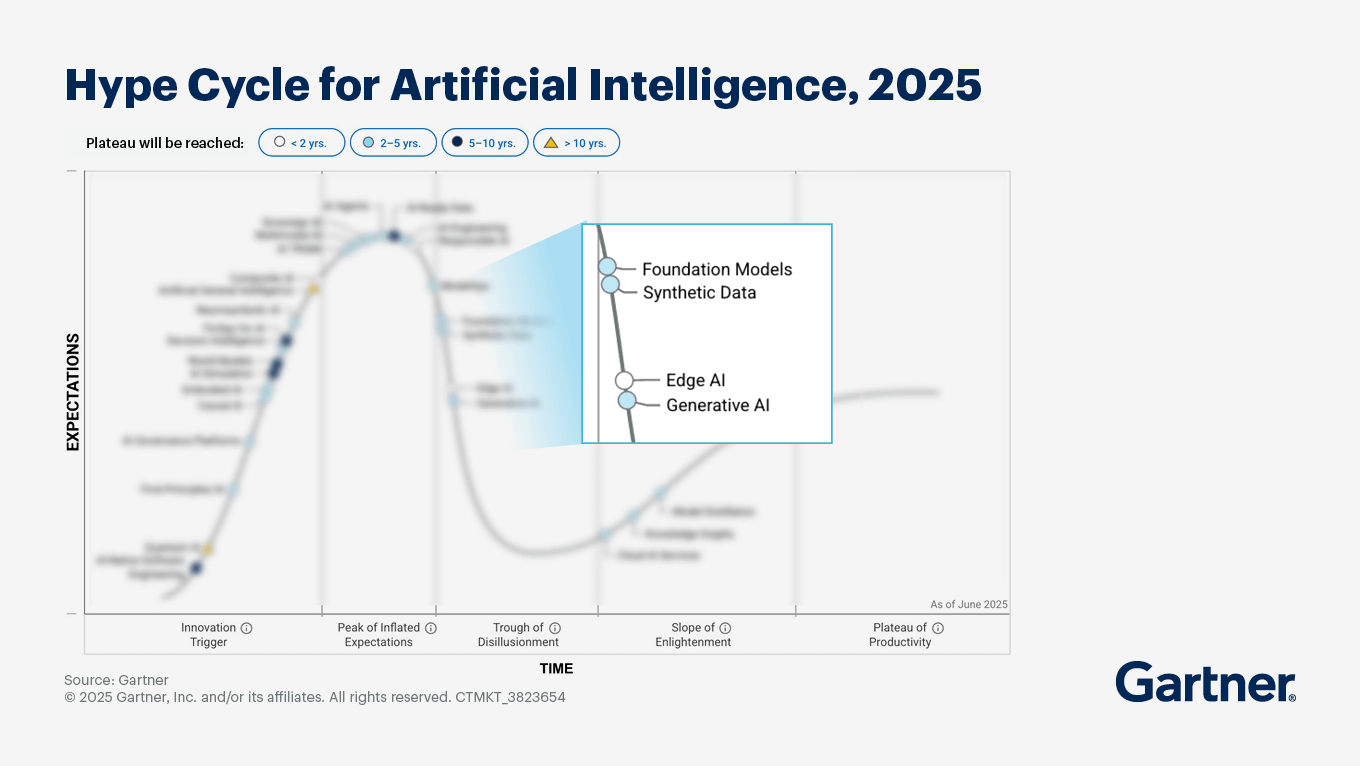

At the same time, Gartner places GenAI in the trough of disillusionment and highlights that companies are spending real money but struggling to see consistent returns. This means on the buyer side enterprise scrutiny is rising, making boards and budgets far less forgiving.

Meanwhile, Gen AI funding overall increased in 2025, but deal volume fell by 35%, indicating more capital is going into fewer, more mature companies. This trend means there is less oxygen for early stage startups that lack differentiation. We expect Gen AI companies that launched and raised capital in 2024 and 2025 will be swallowed by LLM capabilities and will be unable to raise additional capital, meaning we will begin to see these companies fail.

2026 takeaway: If customers can replace a product with a model upgrade, the differentiation was never durable. In 2026, value will accrue to companies with real moats: proprietary data, context orchestration, and distribution. Buoyant believes vertical AI can win (i.e., our investments in HData, Sunairio, and others), but only where it delivers outcomes that horizontal models can’t easily replicate.

4) More Geopolitical and Trade Crises 🌍📉

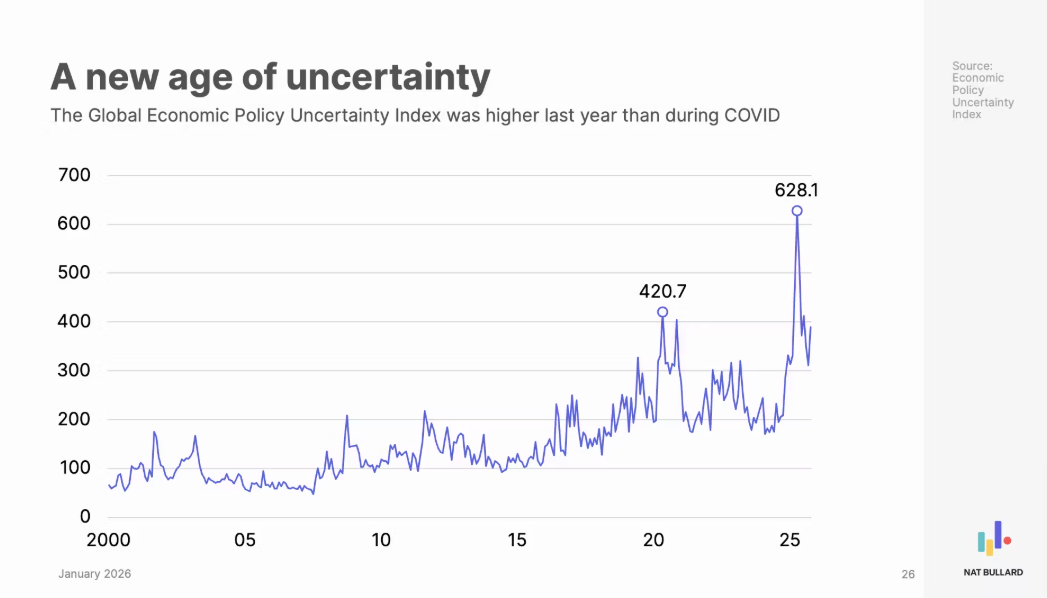

We saw multiple geopolitical crises continue (e.g. Russia / Ukraine) in 2025 and new ones emerge (e.g. US / Venezuela) in early 2026 as well as an all-time high for global economic policy uncertainty as shown in the chart below. And there is no indication that this will let up in 2026. The question is not if there will be more uncertainty, it’s where it’ll come from – which crises can we expect next?

In 2025, the US implemented trade policy that everyone thought wouldn’t last. According to the Yale Budget Lab, this has led to the highest effective tariff rate (18.3%) on US consumers in 90 years. And while tariffs already implemented are being challenged in the courts, there’s no letting up on the US using tariffs to assert its power (e.g. against EU countries for their stance on Greenland). As a result, resilience is becoming a core competitive advantage: overexposure to one geography, one supplier base, or one market will become a greater source of risk.

2026 takeaway: Uncertainty prevails. Resilient companies outperform, and geographic redundancy becomes a competitive moat on both supply and demand.

5) Robotics Leave Pilot Mode 🤖📦

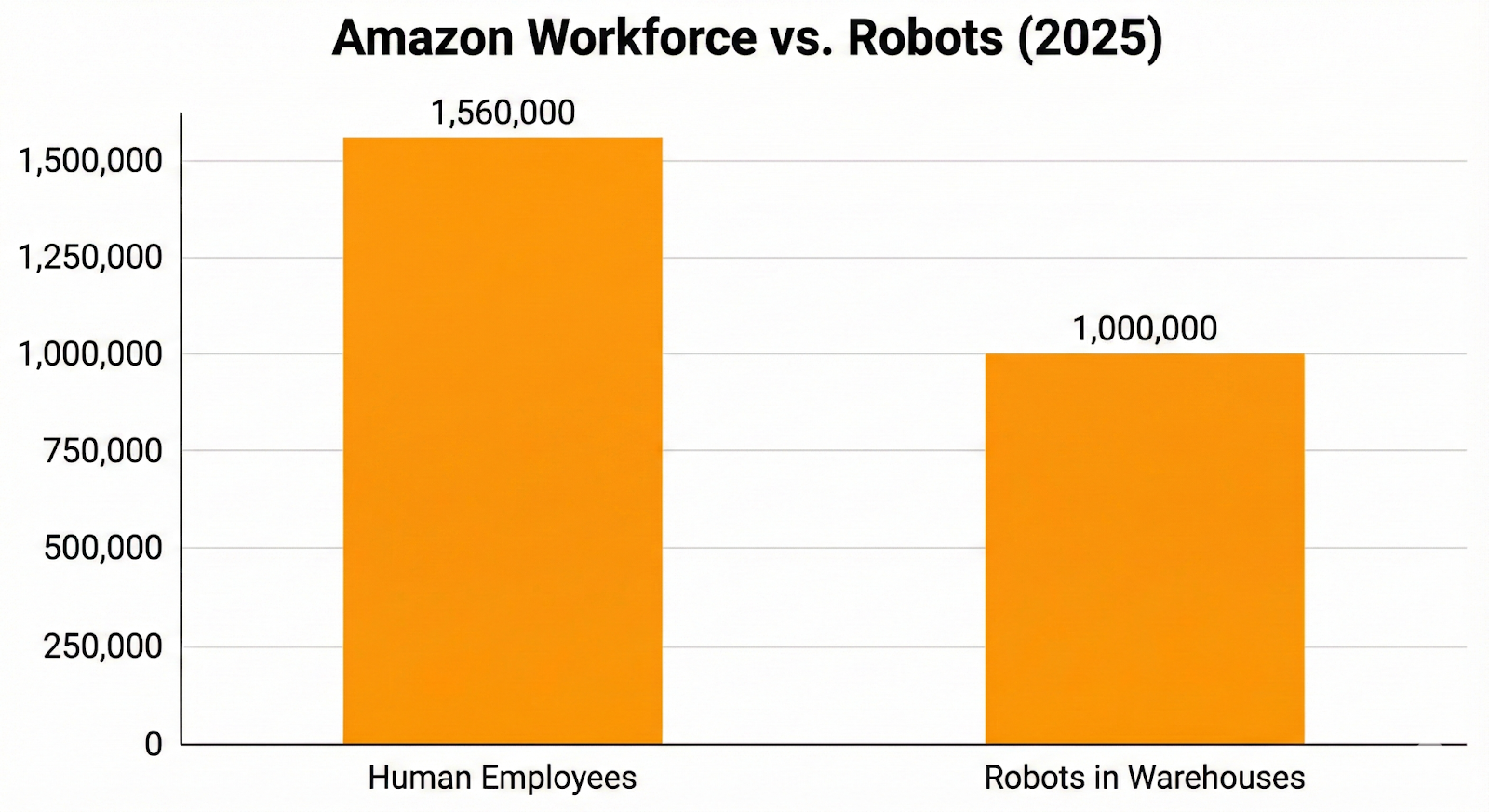

In 2026, robotics adoption moves from pilot programs to scaled deployments in logistics and industrial environments. This is being driven by a combination of labor constraints and the maturity of warehouse automation platforms. Operator behavior shows this is already real at scale: Amazon alone has deployed more than one million robots in its operations after 10+ years of ramp up, and Uber is planning to launch robotaxi service in 2026.

As deployments scale, architectures shift. More systems rely on local inference because edge computing improves time-sensitive robotic execution by reducing latency and enabling real-time processing near the point of action. This pushes more computing to the edge.

We also expect the proliferation of robotics will not immediately cause mass labor displacement; most deployments augment constrained workforces and improve throughput and safety.

2026 takeaway: Robotics becomes an operating strategy (beyond an innovation project), while humanoids remain largely hype relative to ROI. Expect to see major deployments of robotics beyond first movers like Amazon in 2026 and beyond. Also expect to see edge computing as a major theme ahead.

6) A Major AI Security Incident Rattles Enterprise Customers 🔐🧠🚨

AI expands the attack surface, and in 2026 we expect the ecosystem to learn that lesson the hard way.

We believe a major security incident is likely, either through a breach at a foundational model provider or a high-profile rogue agent event where an agent exposes information it shouldn’t. This could look like:

- An agent accidentally leaking sensitive internal documents into logs, vendor workflows, or downstream tools during task execution (for example: copying internal strategy docs into an external ticket or sharing restricted files into a third-party system).

- A model exposing proprietary customer data, such as API-connected enterprise workflows where data is unintentionally retained, surfaced, or accessed across customers due to misconfiguration or vulnerability like this Open AI bug.

- A prompt injection attack where an attacker sneaks new instructions into content, so the AI follows the attacker’s instructions instead of the app’s instructions as described in this academic paper.

- An agentic accidentally deletes a large amount of sensitive data in a way that cannot be recovered and must be reported to the market.

The rush to “AI-everything” has often bypassed traditional corporate IT protocols, and many enterprises are racing to create suitable policies that can manage risk. When a serious incident happens, we expect a sharp short-term chilling effect on adoption, especially for regulated industries like energy and banking, and increased demand for sovereign AI, on-prem deployments, and auditability.

2026 takeaway: A single visible breach changes buyer behavior. Security becomes a gating function for AI adoption, and the winners are the platforms that level up enterprise quality solutions.

7) Grid Software Steps in to Solve Speed-to-Power Challenges ⚡🖥️

The power grid is coming under increasing pressure. According to the EIA, 2024 had double the number of outages compared to the average over the previous ten years. We don’t have official figures for 2025 yet, but anecdotally there have been multiple outages like the recent one in San Francisco that affected more than 100k homes.

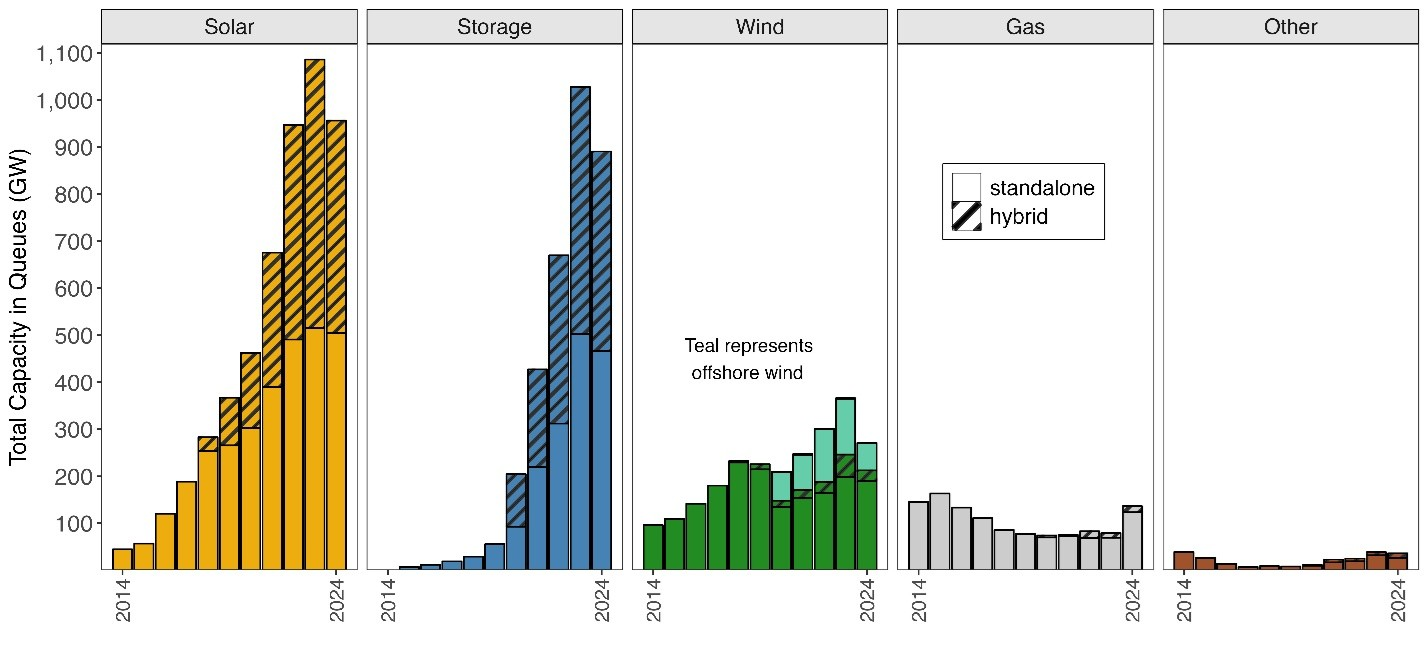

At the same time, interconnection backlog continues with the Lawrence Berkeley National Lab reporting 2,300GW of capacity seeking interconnection and Grid Strategies shows that congestion charges have increased from historical averages around $5B to over $10B in recent years.

More is being invested in transmission as a result. S&P Global shows that planned transmission projects increased 25% in 2025 and utilities combined capex was $84.9B. But physical infrastructure will take time to come online.

In the meantime, utilities and ISOs will move from piloting grid software to implementing it so that it can be a meaningful part of the solution, buying time for infrastructure to be built. We’ll see solutions that provide dynamic line ratings and flexible interconnection that allow utilities to make the most of the physical infrastructure that already exists.

2026 takeaway: This is the year grid software moves from pilot to platform. Procurement replaces experimentation.

8) Investors Called for Liquidity and Markets Answer 📈🔄

If geopolitics don’t ruin the party, markets will deliver sought after liquidity to private and public investors. The returns will be driven by IPOs, corporate M&A, SPACs, and Secondaries.

- Big IPOs to watch for – SpaceX, OpenAI, Anthropic, Discord.

- M&A - big corporates buying vertically integrated AI companies like Microsoft’s acquisition of Nuance in the medical field. We expect to see similar activity in the energy field to continue like Google’s acquisition of Intersect Power.

- SPACs are back, and these are not the SPACs from a few years ago. Expect infrastructure plays and roll-ups, not science projects. SpacInsider tracked 2025 volume that was 3x 2024, and 2026 is off to a strong start.

- Secondaries are projected to grow to over $200B globally in 2026. This is up from $120B in 2025.

Meanwhile, later-stage venture funding concentrates into companies that can prove long-term durability and profitability. As in 2025, companies that demonstrate capital efficiency and profitability will be the most successful in fundraising and selling in 2026.

2026 takeaway: Liquidity improves, but only for companies with real fundamentals. Great companies go public; good companies get acquired.

9) Cities at the Forefront of Climate Risk and Innovation 🏛️🌡️

Municipalities bear the brunt of climate risk as they pay for disaster relief and face lower revenues as natural disasters impact property prices and taxes – 61% of revenue comes from property taxes according to Pew. The impact on cities is exacerbated by the pullback in federal disaster response funding. For example, Bloomberg reported that FEMA lost a $3.3B pool of funds for helping municipalities rebuild after natural disasters.

The silver lining is that the increasing number of natural disasters impacting cities means there is now more clear evidence of the cost, and importantly, the ROI of mitigation efforts. We all know about NIBS’ “theoretical” 6:1 number ($1 invested in mitigation saves $6 in disaster response), but now it is playing out in practice.

We think this will catalyze innovation at the city-level, including practical climate technologies like heat mitigation, flood management, water systems, and climate analytics.

2026 takeaway: Adaptation and resilience become municipal procurement priorities. Climate buying shifts from narrative to necessity. Buoyant has embraced adaptation as a critical part of climate-tech since our founding in 2020, and now we’re seeing this play out and get the attention it deserves.

Closing Thoughts

So what does this mean for climate in 2026? We believe climate investing remains durable, but increasingly pragmatic. In 2025, we saw a slight uptick in climate funding alongside a decline in the number of deals, signaling that more capital is being concentrated into fewer, more competitive companies. We also saw data center and energy adjacent verticals attract outsized rounds, reflecting how tightly climate outcomes are now linked to broader industrial and AI-driven demand.

In 2026, capital will favor energy infrastructure, grid resilience, and data center–adjacent decarbonization, while policy-driven or theoretical climate companies face headwinds. The convergence between AI growth and energy demand makes this shift unavoidable, and it reinforces a broader reset in the category: the strongest climate companies will increasingly be defined by business fundamentals first, with climate as a powerful tailwind rather than the core pitch.

We also expect venture funding for climate companies to remain concentrated in the U.S., even as Europe maintains more favorable climate policy and stronger demand signals for adoption. The result is a familiar pattern: climate companies get funded in the U.S., then build commercial momentum by selling into global markets.

Ultimately, 2026 will be about who can scale responsibly, profitably, and defensibly in a world where physical constraints matter again.

Related Posts

Subscribe to stay updated on news, insights, & invites to special events within our community.

We’re lighting the path forward for the ClimateTech industry—keep up with us along the journey.